Introduction

Start-ups aim to bridge market gaps with innovative products and services, and the availability of capital is crucial for their growth. Given their limited revenue and high failure risk, start-ups often face challenges raising funds. To overcome these, many opt for a hybrid investment tool known as convertible debt or convertible note. This tool allows investors to initially lend money as a loan, which can later be converted into company shares, thus making the investor a shareholder. Convertible debt has gained popularity due to its dual benefits: start-up founders can avoid premature equity dilution while securing funding, and investors receive interest on their loan with the option to convert it into ownership without extra cost. This flexible funding method has led to increased regulatory attention, with governments updating frameworks to facilitate its use. This article will explore the legal aspects and compliance requirements for start-ups issuing convertible debt, provide recent examples of businesses utilizing this tool, and discuss its tax implications. Additionally, it will suggest regulatory improvements to streamline investments through convertible debt.

What is a Convertible Debt?

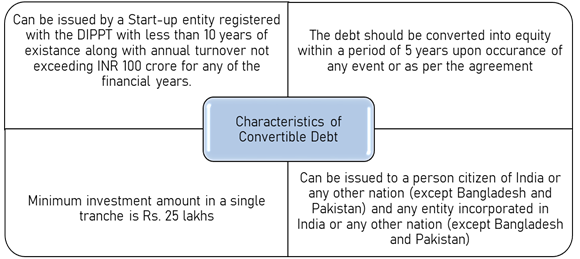

A convertible debt or convertible note has been defined under the Non-Debt Instruments (NDI) Rules, 2019 as a financial instrument issued by a start-up company acknowledging receipt of money initially as debt, repayable at the option of the holder, or which is convertible into such number of equity shares of that company within a period not exceeding five years from the date of issuance of the convertible note.

Legal Provisions Related to the Issuance of Convertible Debt in India

Convertible debt is regulated by the Securities and Exchange Board of India (SEBI) and the Reserve Bank of India (RBI), with key provisions outlined in:

– Companies Act, 2013: Section 62(3) of the act mandates a special resolution to be passed by the company prior to issuing debt options that are later convertible into equity of the company. Moreover, such issuance shall not increase the subscribed capital of the company.

– Companies (Acceptance of Deposits) Rules, 2014: Section 2(c)(ix) of the rules exempts any amount raised by a start-up company via convertible debt from the ambit of ‘deposits’. This exemption results in less paperwork and makes convertible debt an attractive investment tool for new-age businesses.

– Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2017: The Reserve Bank of India, via notification no. FEMA 20(R)/2017-RB, introduced regulations concerning the issuance of convertible debts or notes to foreign persons. Section 8(2) of the regulations comprehensively mandates a start-up company engaged in a sector where government approval is mandatory for foreign direct investment (FDI) to secure such approval before issuing such convertible debt to foreign persons. Moreover, the conversion of debt into equity shall be in accordance with sectoral caps, entry routes, pricing guidelines, and other conditions for foreign investment. If the deposit has been made in foreign currency, then the start-up must report such inward flows to the authorized dealer bank in a convertible note (CN) within 30 days.

– Foreign Exchange Management (Deposit) Regulations, 2016: Schedule 5 of the regulations govern provisions for opening an escrow account. This escrow account can be utilized to receive foreign inward remittances after issuing convertible debt to foreign persons. The consideration for issuing these instruments can also be received in the Foreign Currency (Non-Resident) Accounts (FCNR) or the Non-Resident External Account (NRE) maintained in accordance with the regulations. These regulations collectively streamline the process and compliance for start-ups issuing convertible debt.

Taxation on Convertible Debt

Convertible debt instruments were introduced to attract both foreign and domestic investments into the start-up ecosystem with a simplified taxation regime, facilitating the smooth entry and exit of foreign capital. Under the Income Tax Act, 1961, these instruments are treated as capital instruments, with specific provisions for both start-ups and investors:

– For Startup: Convertible notes are treated as debt instruments under the Income Tax Act, 1961, and therefore, interest paid on such loans is considered a business expense deductible for tax purposes. Moreover, pursuant to Section 47(x) of the Act, the conversion of debt into equity options is exempt from capital gains tax.

– For Investors: For the investor, interest received on such instruments is considered income from other sources under § 56 of the Act, and other capital gains taxes are accrued once the converted shares are sold. During the time of conversion, if the shares are exchanged at a higher rate than the fair market value of the company, the excess amount, or the difference between the conversion rate and the market rate, is treated as income from other sources under § 56(2)(x) of the act.

Regulatory Compliance and Procedure

A startup’s board of directors or partners must give its approval before issuing a convertible note. Following an extraordinary general meeting to secure shareholder approval, e-form MGT-14 must be submitted to the MCA within 30 days. The issuance and subscription of the note, closing deliverables, rights of parties, conversion terms (including price, events, and interest rates), and transfer limitations are all covered in the next stage, which is to prepare and execute a convertible note agreement. If the money is coming from people outside of India, one must file form CN with the RBI and ascertain if the remittance is subject to approval or the automatic route. Additionally, the RBI requires a yearly report in form FLA from Indian startups that receive foreign direct investment.

Valuation and Conversion

Under Indian FDI regulations, a valuation report is required when converting a convertible note into shares, although it is not necessary when issuing the note. After ten years or upon certain events, holders of convertible notes may convert to equity shares. In such a case, they will receive shares at a predetermined valuation and the startup will issue shares in accordance with legal procedures. Holders may also choose to redeem their note, in which case they would get greater interest rates because the note is still a debt until conversion. Either the valuation at the time of conversion or a predetermined valuation at issuance serves as the basis for the conversion ratio. In order to get capital without premature stock dilution, startups and foreign investors might agree on terms for the issuance of convertible debt, which starts out as a loan and later converts to equity based on a predetermined formula or a discount on the company’s market value.

Conclusion

Convertible notes serve as a valuable financing tool for India’s expanding startup ecosystem. By comprehending and complying with the legal terms for issuing these notes, entrepreneurs can secure essential investments and foster their startup’s development. Regulations and compliances for convertible debt have evolved significantly, spurred by the government’s active promotion. One key improvement is the extension of the conversion period from 5 to 10 years, demonstrating efforts to streamline the process and foster a favorable environment for issuing convertible debt in India. However, the regulations are scattered across various rules and circulars by different agencies, making it challenging for businesses and investors to stay informed. To address this, the Department for Promotion of Industry and Internal Trade (DIPP) should issue a comprehensive report detailing all legal norms for the issuance and redemption of convertible debt, incorporating feedback from start-ups. Additionally, amending specific sections of the Companies Act, 2013, and the Income Tax Act, 1961, to include a clear framework for convertible debt could reduce existing ambiguities and enhance clarity for all stakeholders.