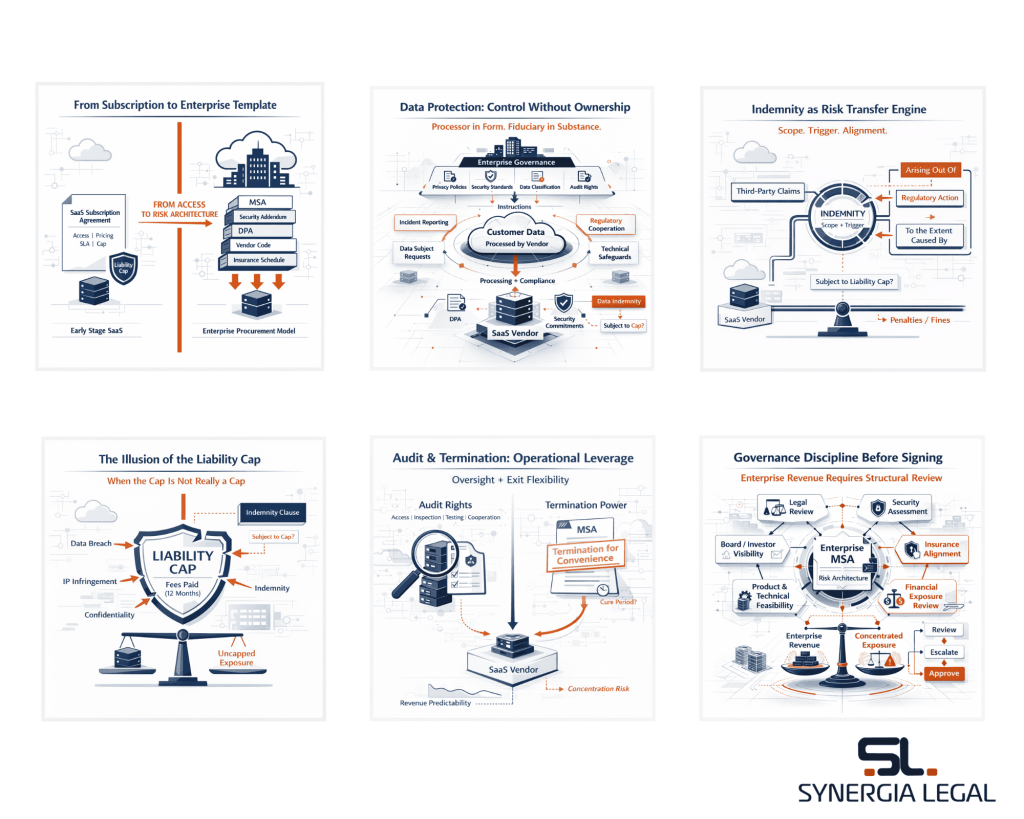

In the early stages of growth, most software-as-a-Service (“SaaS”) ventures contract on their own subscription term, concise agreements built around standard access rights, pricing tiers, basic service levels and a capped liability construct aligned with annual fees. The commercial discussion typically centres on scope, implementation timelines and payment cycles. Legal risk, while present, remains proportionate to the scale of engagement.

The dynamic changes materially once a startup begins contracting with large enterprises. The document is no longer a subscription agreement but a procurement-driven master services agreement (“MSA”), accompanied by layered schedules, security addenda, data processing terms and vendor codes of conduct. The starting point is not balance, but risk containment from the enterprise’s perspective.

Enterprise MSAs are structured to allocate operational, regulatory and third-party risk downstream to the vendor. Definitions are broadened, warranties are expanded and indemnities are drafted to anticipate scenarios far beyond routine service delivery. Clauses that appear standard in isolation, unlimited liability carve-outs, audit rights, termination for convenience, assume greater significance when read together as part of a coordinated risk framework.

For Indian startups transitioning into enterprise contracting, the legal exercise therefore shifts from documenting access to software, to assessing exposure concentration. Revenue visibility must be evaluated alongside liability architecture. The enterprise deal is no longer merely a commercial milestone; it is a structural redefinition of contractual risk.

Understanding the Enterprise Template: Where Risk Is Quietly Reallocated

Enterprise MSAs are rarely neutral starting points. They are standardised procurement instruments developed to ensure uniform risk containment across vendors. While presented as “standard terms”, these templates are structured to shift operational, regulatory and third-party exposure downstream to the service provider. The reallocation of risk is seldom dramatic; it is embedded incrementally through drafting technique and document layering.

Risk often expands at the definitional stage. “Services” may be drafted broadly to include implementation support, integration assistance, advisory inputs and ancillary deliverables. This widens performance expectations beyond core SaaS access. Similarly, obligations to comply with “all applicable laws relating to the Services” can indirectly incorporate sector-specific regulations applicable to the enterprise customer. Where “Customer” is defined to include affiliates, exposure may extend across group entities without corresponding commercial upside.

Enterprise engagements typically involve multiple interconnected documents, the MSA, statements of work, security addenda, data processing terms, vendor codes of conduct and insurance schedules. Material obligations often reside outside the main body of the MSA. Detailed security controls, incident reporting timelines, audit cooperation clauses and regulatory flow-through obligations may be embedded in annexures that are treated as boilerplate but carry substantive risk.

Certain provisions operate cumulatively. Liability caps may appear commercially aligned, yet carve-outs in indemnity, confidentiality or data protection clauses dilute their practical effect. Audit rights, termination for convenience and expansive warranties further concentrate exposure.

An enterprise template must therefore be read holistically. The question is not whether a single clause is acceptable in isolation, but whether the integrated framework results in disproportionate risk relative to revenue.

Liability Caps: When the Cap Is Not Really a Cap

Enterprise MSAs almost invariably contain a headline limitation of liability, typically linked to fees paid over a defined period. At first glance, this provides commercial certainty. In practice, however, the operative exposure depends less on the stated cap and more on the drafting architecture surrounding it.

1. Carve-Out Inflation

The most common erosion mechanism is the proliferation of carve-outs. Data protection breaches, confidentiality obligations, intellectual property infringement, and instances of “gross negligence” or “wilful misconduct” are frequently excluded from the cap. Over time, these exclusions expand to cover the very risks most likely to arise in a SaaS engagement. Where such carve-outs are drafted broadly, without materiality thresholds or knowledge qualifiers, the protection offered by the cap becomes increasingly narrow.

2. Indemnity Misalignment

A recurring structural issue arises where indemnity provisions are drafted independently of the limitation clause. If the agreement is silent on whether indemnities are subject to the cap, enterprises may argue that indemnity obligations stand uncapped. The practical result is that the liability cap governs direct contractual damages, while the most significant third-party claims sit outside it.

3. Revenue–Exposure Imbalance

Liability must also be evaluated against commercial reality. An annual contract value of modest scale may be paired with uncapped exposure for data incidents or IP claims, potentially far exceeding insurance coverage and the vendor’s financial capacity. Where claims may be brought by affiliates or group entities, exposure can multiply further.

The key inquiry is therefore integrated: does the combined effect of carve-outs, indemnities and affiliate rights preserve the economic logic of the cap? A numerical limit in isolation offers little comfort if the surrounding provisions render it largely theoretical.

Indemnity Design: Scope, Trigger and Regulatory Spillover

In enterprise SaaS contracting, indemnity clauses often operate as the primary mechanism for risk transfer. While limitation of liability provisions appear to define financial exposure, indemnities frequently determine where third-party, statutory and regulatory risk ultimately resides. The drafting of scope and trigger therefore warrants careful scrutiny.

1. Scope: What Is Being Indemnified?

Enterprise templates typically extend indemnity beyond intellectual property infringement to include breach of applicable law, data protection violations, confidentiality breaches and even non-compliance with internal policies incorporated by reference. Where the language is framed as indemnifying against “any loss arising out of” a breach, the obligation may capture investigation costs, settlement amounts and, in some instances, regulatory penalties.

In regulated sectors, indemnity language may be expanded further to address supervisory action or compliance lapses linked to outsourced functions. The practical effect is that the vendor assumes exposure not only for its own operational failure, but for regulatory consequences experienced by the enterprise.

2. Trigger: Fault or Strict Allocation?

The distinction between “arising out of” and “to the extent caused by” is commercially significant. The former may operate as a strict allocation of risk, while the latter ties indemnity to demonstrable fault. Equally important is whether indemnity is limited to third-party claims or extends to internal losses and administrative penalties.

Procedural mechanics also shape exposure. Where the enterprise retains unilateral control over defence and settlement, the vendor’s financial exposure may crystallise without meaningful participation in strategy.

3. Regulatory Spillover and Cap Alignment

Indemnity must be read alongside the limitation of liability clause. If not expressly subject to the cap, it may operate as a de facto uncapped obligation. Alignment with available insurance coverage is equally critical. Absent structural coherence, indemnity provisions can transform a commercial services arrangement into a broad guarantee of enterprise compliance.

Data Protection in Enterprise Deals: Control Without Ownership

In enterprise SaaS engagements, data protection provisions frequently become the most expansive and operationally intrusive component of the contractual framework. While the vendor may not own the underlying data, it is often required to assume significant compliance and security obligations in relation to its processing. The allocation of responsibility is therefore less about ownership and more about risk insulation.

1. Processor in Form, Fiduciary in Substance

Enterprise templates typically characterise the vendor as a data processor. However, the contractual obligations imposed may extend well beyond processor-level responsibilities. Broad representations of compliance with “all applicable data protection laws,” assistance with data subject requests, and detailed security commitments can effectively elevate the vendor’s exposure. Simultaneously, enterprises retain control over privacy policies, data classification standards and security frameworks, often incorporating such policies by reference and reserving unilateral update rights.

The resulting structure places operational accountability on the vendor, while strategic governance remains with the enterprise.

2. Security Addenda and Regulatory Flow-Through

Security schedules commonly mandate strict incident reporting timelines, expansive audit rights and adherence to specified technical standards or certifications. In regulated sectors, additional obligations may mirror supervisory expectations applicable to the enterprise, including cooperation with inspections or restrictions on data storage and transfers.

These requirements can extend beyond statutory baselines, particularly where enterprises seek regulator-level oversight parity in vendor contracts.

3. Liability Alignment

Data-related indemnities frequently include investigation costs, notification expenses and, in some instances, regulatory penalties. Where such exposure is uncapped or misaligned with insurance coverage, the commercial balance of the transaction may be distorted.

Enterprise data clauses must therefore be assessed holistically — not merely as compliance instruments, but as concentrated allocations of operational and regulatory risk.

Audit and Inspection Rights: Operational Intrusion Risk

Enterprise audit clauses are typically framed as compliance safeguards. In substance, however, they function as ongoing oversight mechanisms that can materially affect operational autonomy. Unlike financial audits in traditional outsourcing arrangements, enterprise SaaS audits frequently extend into technical, organisational and regulatory domains.

1. Scope Beyond Financial Review

Enterprise templates often grant access to systems, infrastructure, personnel and subcontractor arrangements. Audit language may permit review of security controls, logs, internal policies and compliance documentation. In regulated sectors, such rights can extend to cooperation in supervisory inspections or production of materials aligned with the enterprise’s regulatory obligations.

The breadth of drafting is significant. Audit clauses that are not clearly limited may allow inspection beyond the proportional risk presented by the engagement.

2. Frequency and Procedural Safeguards

Risk intensifies where audit rights are not accompanied by procedural controls. Absence of advance notice requirements, frequency limits or restrictions on business disruption can expose the vendor to recurring operational intrusion. In many templates, audit costs — including remediation expenses — are borne by the vendor, further increasing exposure.

Where technical testing rights such as vulnerability assessments or penetration tests are included, coordination and security controls become critical to avoid unintended system disruption.

3. Regulatory Parity and Confidentiality Concerns

When contracting with regulated enterprises, audit rights may be drafted to mirror regulator-level access. This can result in indirect supervisory oversight without the statutory safeguards ordinarily applicable to regulated entities.

Audit provisions must therefore be assessed in conjunction with confidentiality, liability and termination clauses. Findings from audits may trigger breach allegations or indemnity claims. In enterprise SaaS contracting, audit rights are not passive review tools, they are structural levers that can alter the balance of control within the relationship.

Termination for Convenience and Revenue Stability

Termination provisions in enterprise MSAs warrant close scrutiny, particularly in subscription-driven SaaS models where revenue visibility underpins valuation and operational planning. While pricing and commercial terms may be negotiated over multiple years, termination clauses often preserve unilateral exit flexibility for the enterprise.

1. Termination for Convenience

Enterprise templates frequently permit termination for convenience on short notice, sometimes without minimum commitment or early termination compensation. Where discounted pricing has been structured on the assumption of a multi-year engagement, such flexibility can undermine the economic basis of the deal. The vendor bears upfront onboarding, implementation and infrastructure costs, while the enterprise retains the option to disengage without equivalent financial consequence.

2. Termination for Cause and Broad Breach Triggers

Material breach definitions in enterprise contracts may be expansive, capturing service level deviations, compliance lapses or audit findings. If cure periods are narrowly drafted or operational standards are broadly framed, relatively minor disputes may escalate into termination rights. In regulated sectors, non-compliance allegations linked to supervisory expectations can further widen termination triggers.

3. Revenue Concentration and Investor Implications

Enterprise accounts often represent meaningful revenue concentration. Termination flexibility in top contracts therefore affects not only cash flow predictability but also investor diligence assessments. Investors typically review key customer agreements to evaluate exposure to early exit risk and its impact on recurring revenue stability.

4. Exit and Transition Obligations

Termination is rarely the end of contractual responsibility. Transition assistance, data migration support and ongoing cooperation obligations may extend beyond the revenue stream itself, sometimes at limited or no additional cost.

Enterprise termination clauses should therefore be evaluated in the context of revenue predictability, cost recovery and broader risk architecture. What appears commercially attractive at signing may, without structural balance, introduce disproportionate revenue volatility.

Exclusivity, MFN and Strategic Lock-In

Enterprise contracts frequently extend beyond risk allocation and enter the domain of commercial control. Provisions relating to exclusivity and Most Favoured Nation (MFN) pricing can materially influence a SaaS company’s growth trajectory, pricing architecture and portfolio flexibility.

1. Exclusivity and Market Containment

Exclusivity clauses may restrict the vendor from servicing identified competitors, industry segments or geographic markets. While often presented as a commercial quid pro quo for volume or brand association, such restrictions can constrain expansion into adjacent markets. In some cases, exclusivity is not explicit but arises indirectly through integration commitments, roadmap alignment obligations or pricing structures that make servicing competitors commercially impractical.

For startups building scalable products, even narrowly drafted exclusivity provisions require careful evaluation against long-term market strategy.

2. Most Favoured Nation Clauses and Pricing Rigidity

MFN clauses typically require the vendor to offer the enterprise terms no less favourable than those extended to other customers. While appearing commercially reasonable, such provisions can limit pricing flexibility across different customer segments. A discounted enterprise deal concluded at scale may inadvertently anchor pricing benchmarks for future engagements.

MFN obligations may also create tension with confidentiality commitments, particularly where enterprises seek visibility into comparative commercial arrangements.

3. Strategic Lock-In and Portfolio Risk

Volume-linked pricing without firm minimum commitments, or contractual undertakings to prioritise feature development, can subtly align product strategy with a single enterprise’s needs. This concentration risk may be scrutinised in investor diligence, particularly where revenue from one customer materially influences overall performance.

Exclusivity and MFN provisions should therefore be assessed not only for immediate commercial benefit, but for their long-term impact on scalability and strategic optionality. In enterprise contracting, preserving growth flexibility is as critical as managing liability exposure.

Internal Governance Before Signing Enterprise Contracts

Enterprise MSAs should not be treated as routine sales documentation. Large enterprise engagements concentrate liability, regulatory exposure and operational commitments in a manner that can materially affect a startup’s risk profile. Accordingly, execution should follow structured internal review rather than purely commercial momentum.

1. Exposure-to-Revenue Assessment

Before signing, companies should evaluate the relationship between contractual exposure and economic upside. This includes examining whether liability caps meaningfully correspond to annual contract value, whether carve-outs undermine that protection, and whether indemnity obligations sit within available insurance coverage. Where a single enterprise represents a material percentage of recurring revenue, termination flexibility and audit-triggered breach risk warrant particular attention.

2. Structured Red-Line Discipline

Enterprise negotiations often move quickly once commercial alignment is reached. However, internal clarity on non-negotiable provisions is essential. Preservation of the integrity of the liability cap, alignment of indemnity with limitation clauses, and procedural safeguards around audit rights typically fall within this category. Other elements, such as reporting formats or certain service level adjustments, may be commercially tradable.

Establishing an internal escalation protocol, including when board or investor visibility is appropriate, reduces the risk of last-minute concessions that distort the contractual balance.

3. Cross-Functional Review

Enterprise contracts frequently impose commitments that extend beyond legal risk. Security obligations impact technology teams; insurance thresholds affect finance; compliance representations carry regulatory implications; and product roadmap commitments may influence development priorities. Coordinated review across functions ensures that contractual undertakings are operationally sustainable.

Conclusion

Enterprise SaaS contracts are not merely expanded subscription agreements; they are structured risk allocation frameworks. Liability caps, indemnities, audit rights and termination provisions must be read together to assess their cumulative impact.

For growing SaaS businesses, enterprise revenue signals maturity. That maturity must be reflected in disciplined contractual governance. Sustainable scale is achieved not only by securing marquee customers, but by ensuring that the legal architecture supporting those relationships remains commercially proportionate and strategically aligned.